))

Episode 38: Episode 38 – New Property Insurance Reforms

Manage episode 332417617 series 3032177

Контент предоставлен The Florida Insurance Roundup from Lisa Miller & Associates and The Florida Insurance Roundup from Lisa Miller. Весь контент подкастов, включая эпизоды, графику и описания подкастов, загружается и предоставляется непосредственно компанией The Florida Insurance Roundup from Lisa Miller & Associates and The Florida Insurance Roundup from Lisa Miller или ее партнером по платформе подкастов. Если вы считаете, что кто-то использует вашу работу, защищенную авторским правом, без вашего разрешения, вы можете выполнить процедуру, описанную здесь https://ru.player.fm/legal.

The Florida Legislature in a May special session passed a series of reforms to help stabilize a property insurance market that has seen a growing number of carriers stop writing business or becoming insolvent. Homeowners rates keep growing by double-digits and coverage is increasingly difficult to obtain.

Former Florida Deputy Insurance Commissioner Lisa Miller talks with a lawmaker who was one of the handful of leaders behind the reforms and the head of a litigation analytics firm on whether the two new laws will help re-right the marketplace and lower homeowners rates - and what further reform is most needed next.

Show Notes

Florida’s newest property insurance and consumer reforms build on legislation passed in 2019 and 2021. The two new laws (SB 2-D & SB 4-D) target excessive litigation, contractor solicitation abuse, and provide $2 billion in no-cost reinsurance coverage to carriers to improve the affordability and availability of insurance coverage. More than 12 companies have stopped writing new business since January. Another seven companies have become insolvent since 2019 - six in just the past 12 months.

“This was a matter of first aid to save a dying patient, which was Florida's property insurance market but there's absolutely still more to do,” said Representative David Smith (R-Winter Springs) who supported the two bills that became law and took effective immediately on May 26, 2022. “There are some homeowners that the legislation is going to help immediately. But longer term, I think homeowners will see lower rates and an impact of the rates going up less because of the stabilization of the market….we’re on the right track.”

According to the National Association of Insurance Commissioners’ data, as reported by state Insurance Commissioner David Altmaier, Florida has 9% of all homeowners insurance claims in the US yet has 79% of all homeowners insurance claims lawsuits. The number of property insurance lawsuits in the state has increased 363% in the past nine years. The current excesses are driven by fraudulent roof claims.

“A lot of the new measures are litigation related with the intent that either the laws will reduce the lawsuit amounts or reduce the cost of each lawsuit to the insurance industry, which would then translate to lower insurance premiums for Floridians,” said Wesley Todd, CEO of CaseGlide, a Tampa-based litigation analytics and software firm serving the insurance industry. He noted the real question is exactly when rates will come down given the reforms will take time to be reflected in renewal policies over the coming months. Insurance companies and their reinsurers will then want to see “years of data” that suggests litigation costs are under control. “I believe that lawmakers still have one more thing left to do, which is get rid of the attorney fees statute, which is the structure that incentivizes attorneys to sue insurance companies. I think until they do that, we won’t actually start to see rates for Floridians decrease.”

Florida’s attorney fees statute (627.428 f.s.) requires an insurance company pay attorney fees when the policyholder prevails in a lawsuit against the company. It has helped in catastrophes such as 1992’s devastating Hurricane Andrew, to encourage representation “so that consumers would have a level playing field,” host Miller said. “What has happened is that there are contractors who use that statute to their own benefit and will have their favorite partner, a plaintiff lawyer, and they become a team, once the consumer is kind of marginalized, if you will.”

Rep. Smith said the new reforms prohibit awards of attorney fees to contractors or other assignees of an Assignment of Benefits (AOB) contract. “Again, we've got to do more. And the legislature never wants to deny the consumer, that homeowner the ability to get an attorney and be represented and get their day in court,” he said. While Florida has weather issues to deal with that can impact insurance rates, “it's the litigation costs that are driving these rates up and why reinsurance companies don't want to take the actuarial risk of having all this litigation in Florida. It's not the hurricanes they fear, it’s the trial lawyer,” Rep. Smith said.

Todd agreed and said the “surgical approach” the legislature rightfully utilized in the 2019 and 2021 reforms was meant to solve the litigation problem without getting rid of the attorney fees statue, but that hasn’t worked. “If we put a lot of loopholes and obstacles in front of the plaintiff attorneys, but they get paid to jump through those loopholes because they get paid for all their attorney fees, then are they really obstacles? They're things that actually create more revenue for the attorneys because they're being paid to jump through hoops,” Todd argued.

“It’s not the $35,000 roof that is the burden on the insurance company,” added Rep. Smith. “It’s the $150,000 or $200,000 in attorney fees that they get paid. That’s what creates the litigation risk.” He discussed his idea of creating a blue ribbon commission to meet outside the time constraints of the legislature’s annual 60-day session and five weeks of prior committee meetings to collect data, benchmark other states’ efforts, and “to get everybody that has a vested interest in solving the problem to everybody that’s part of the problem to come together to be part of the solution,” Rep. Smith said. In the meantime, Senator Jim Boyd (R-Bradenton) who chairs the Insurance and Banking Committee is expected to hold workshops this summer to provide more information and data that some lawmakers complained they didn’t have during the special session.

Host Miller and her guests also discussed what wasn’t in the new reform laws: Citizens Property Insurance Corporation, the state-created and taxpayer-backed “insurer of last resort.” Its policy count is rapidly approaching one million as private insurance companies have gone insolvent or shed policies because of underwriting losses. It under-market rates and growing policy count burden will subject the rest of Florida’s policyholders across almost all insurance lines (including automobile & surplus lines) to pay a special assessment if Citizens runs out of money to pay claims, as it did during the spate of 8 hurricanes during the 2004-2005 season.

Host Miller agreed with both of her guests that the legislature needs to eliminate the attorney fees statute. She said lawmakers should also go beyond the roof deductible option that consumers can access as part of the new law and instead require actual cash value for roof replacement as 40 other states do. She also advocates for elimination of AOB contracts and reform of the Florida Hurricane Catastrophe Fund that could save homeowners an estimated average $150 a year on their premium.

Links and Resources Mentioned in this Episode

SB 2-D & SB 4-D (bills covering the 2022 reforms)

Final Special Session 2022 Florida Legislature Bill Watch (Lisa Miller & Associates)

Florida Statutes section 627.428 (on attorney fees)

Top 20 Attorneys Filing Property Insurance Lawsuits - 2022 Q1 (Florida Department of Financial Services, April 2022)

Florida Insurance Industry’s Litigation, 2013-2021 (Citizens Property Insurance Corporation)

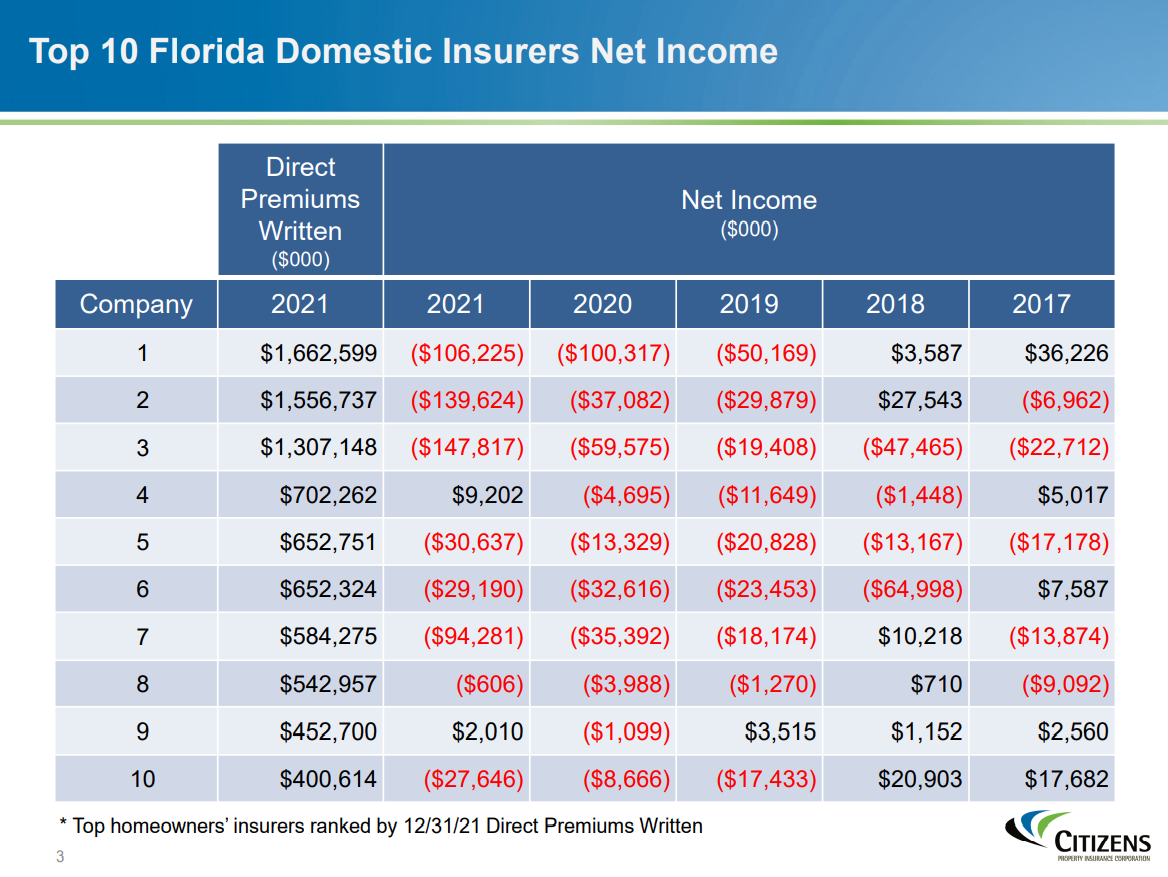

Top 10 Florida Domestic Insurers Net Income Losses (from Citizens Property Insurance Corporation, March 2022)

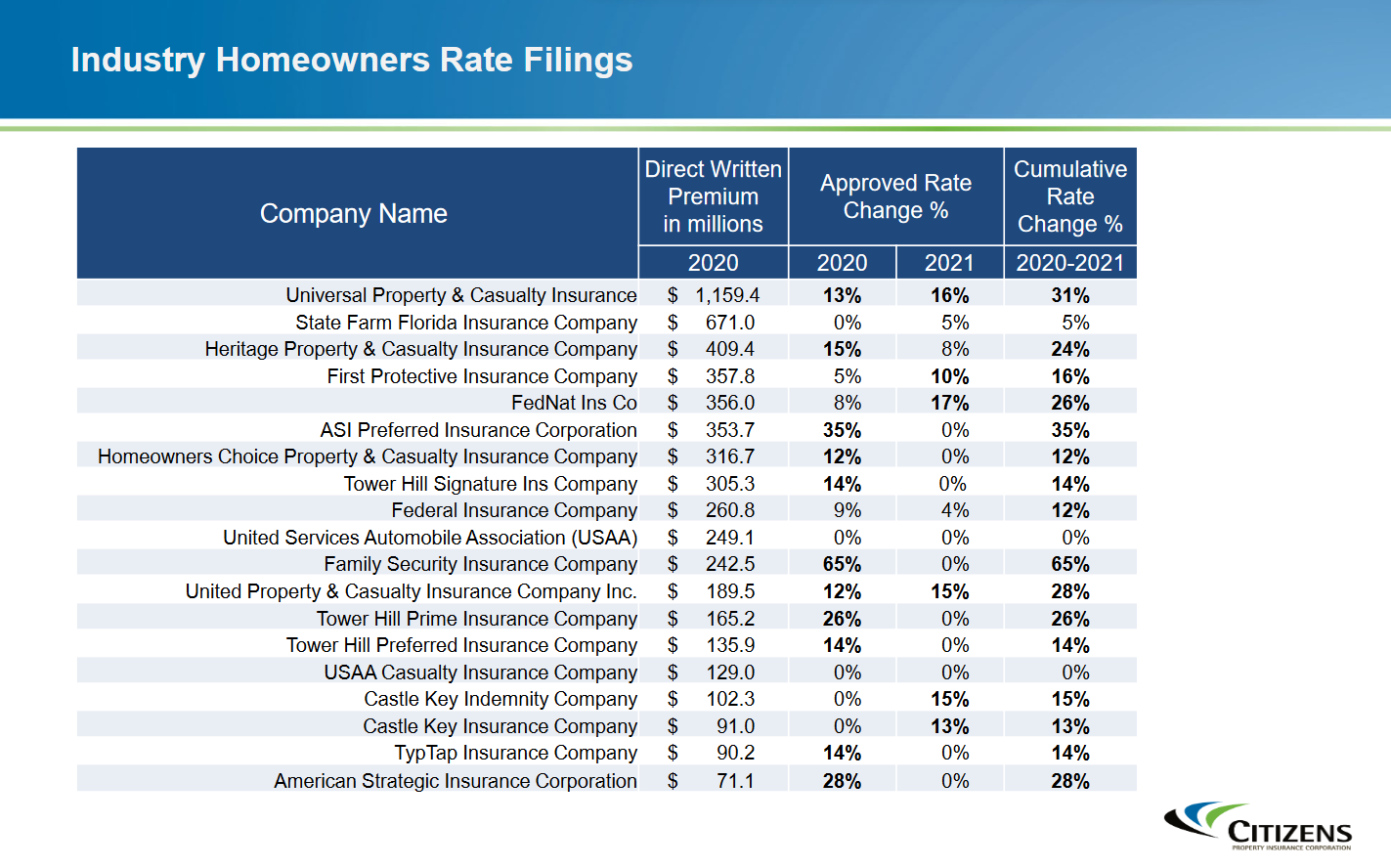

Private Insurance Industry Cumulative Rate Filings 2020-2021 (from Citizens Property Insurance Corporation, March 2022)

Florida’s 2019 AOB Reform (HB 7065) (Lisa Miller & Associates)

Florida’s 2021 Litigation & Solicitation Reform (SB 76) (Lisa Miller & Associates)

Florida’s 2022 Litigation Reform & Consumer Protections (SB 2-D & SB 4-D) (Lisa Miller & Associates)

CFO/Department of Financial Services Insurance Consumer Helpline (1-877-693-5236)

** The Listener Call-In Line for your recorded questions and comments to air in future episodes is 850-388-8002 or you may send email to LisaMiller@LisaMillerAssociates.com **

The Florida Insurance Roundup from Lisa Miller & Associates, brings you the latest developments in Property & Casualty, Healthcare, Workers' Compensation, and Surplus Lines insurance from around the Sunshine State. Based in the state capital of Tallahassee, Lisa Miller & Associates provides its clients with focused, intelligent, and cost conscious solutions to their business development, government consulting, and public relations needs. On the web at www.LisaMillerAssociates.com or call 850-222-1041. Your questions, comments, and suggestions are welcome! Date of Recording 6/22/2022. Email via info@LisaMillerAssociates.com Composer: www.TeleDirections.com © Copyright 2017-2022 Lisa Miller & Associates, All Rights Reserved

54 эпизодов

{kind=link}

{kind=link}